LOS F and G requires us to:

f. calculate and interpret portfolio standard deviation

g. describe the effect on a portfolio’s risk of investing in assets that are less than perfectly correlated

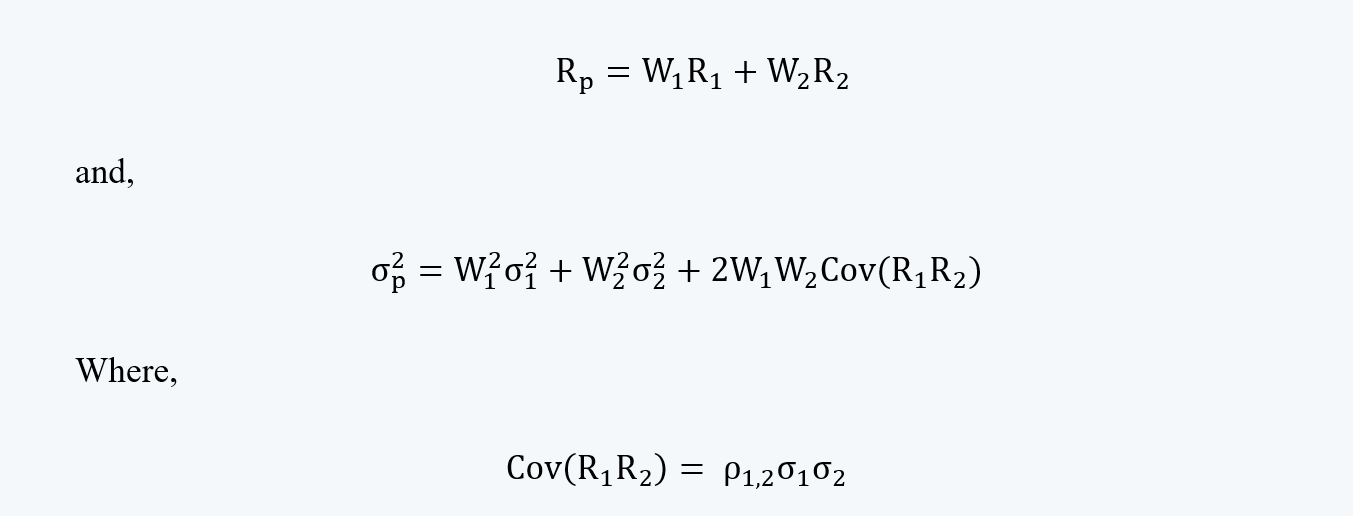

a. As discussed, the portfolio returns and the portfolio standard deviation can be calculated using the formulas:

Here ρ1,2 is the correlation between the two securities. It determines the effect on portfolio risk when two or more assets are combined.

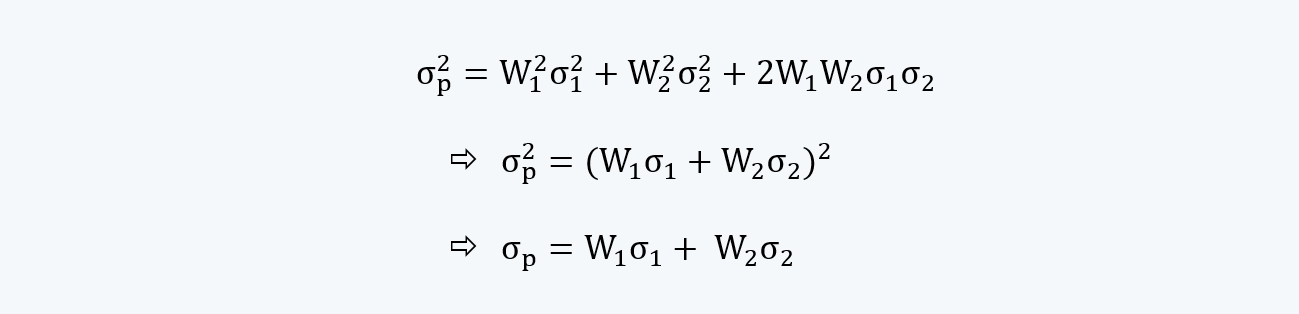

b. For example, if there is a perfect correlation between the two securities in a two-security portfolio, i.e. ρ1,2=1, then

Thus, in the case of perfect correlation, the standard deviation of the portfolio is nothing but the weighted average of the individual risk.

c. Now, let us consider a case of less than perfect correlation between the two assets in a two-asset portfolio, i.e. ρ1,2<1, then

2W1W2 ρ1,2 σ1 σ2 < 2W1W2 σ1 σ2

and, the first part of the equation (i.e. W12σ12 + W22σ22 ) remains the same. Thus, the standard deviation of the portfolio, with perfect correlation is less than the standard deviation of the portfolio with less than perfect correlation.

d. We can explain this with the help of an example:

Suppose there is a two-asset portfolio with both the assets having a return of 10%, a standard deviation of 20%, and equal weight.

i. Now, if the correlation coefficient of the two assets is one, i.e. ρ1,2=1, then:

Rp = 0.5 × 0.10 + 0.5 × 0.10

Rp = 0.10 or 10%

And,

σp2 = (0.5)2 × (0.2)2 + (0.5)2 × (0.2)2 + 2 × 0.5 × 0.5 × 1 × 0.2 × 0.2

σp = 0.20 or 20%

ii. If there is no correlation between the two assets in the portfolio, e. ρ1,2=0, then:

Rp = 0.5 × 0.10 + 0.5 × 0.10

Rp = 0.10 or 10%

And,

σp2 = (0.5)2 × (0.2)2 + (0.5)2 × (0.2)2 + 2 × 0.5 × 0.5 × 0 × 0.2 × 0.2

σp = (0.02)1/2 or 14.14%

iii. Now, if the correlation coefficient of the two assets is a negative one, i.e. ρ1,2= -1, then:

Rp = 0.5 × 0.10 + 0.5 × 0.10

Rp = 0.10 or 10%

However, in the real world, if there are two assets in a portfolio, which are perfectly negatively correlated, having equal weights, then the returns of that portfolio should be zero.

And,

σp2 = (0.5)2 × (0.2)2 + (0.5)2 × (0.2)2 + 2 × 0.5 × 0.5 × (1) × 0.2 × 0.2

σp = 0

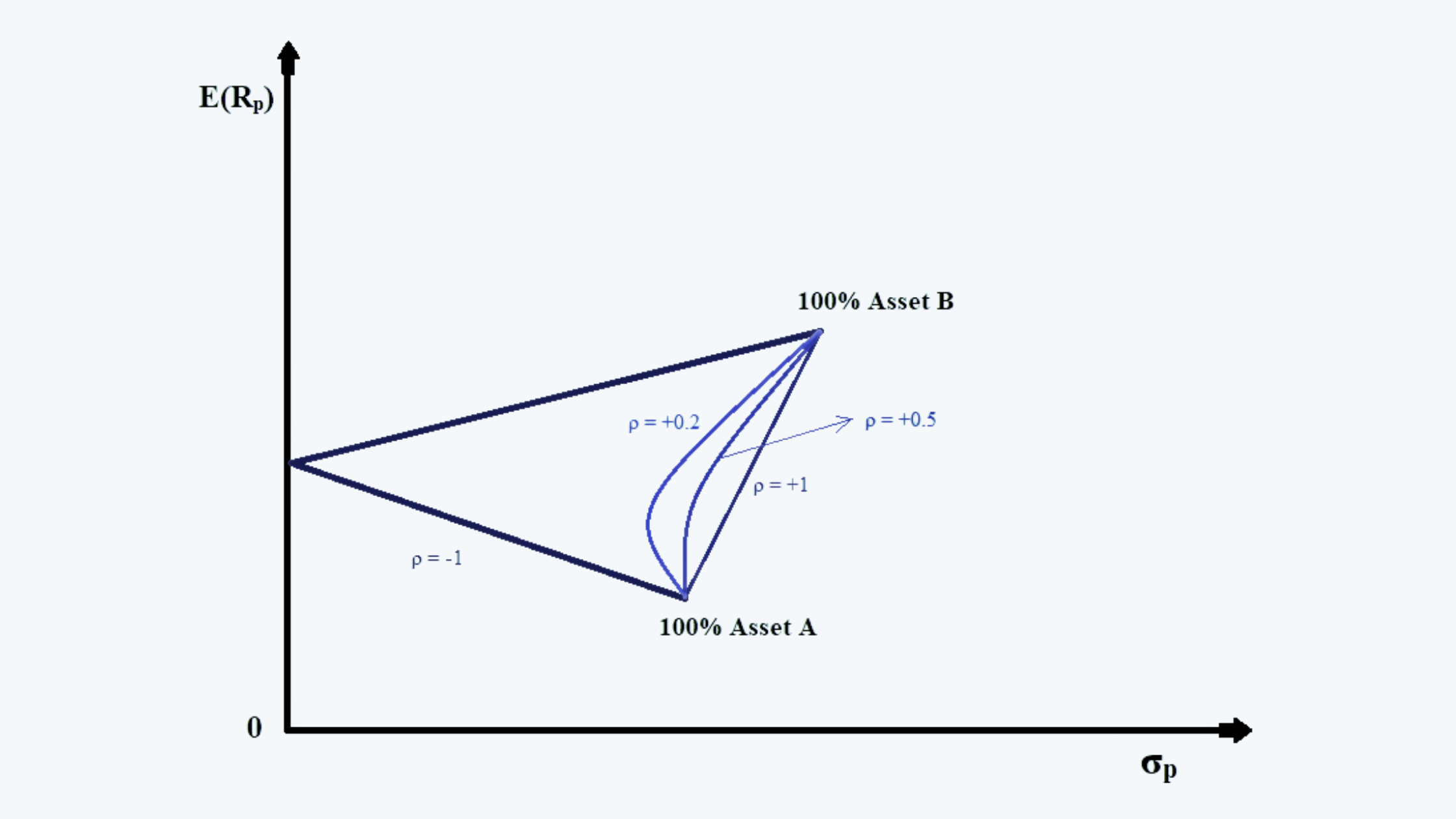

e. Suppose we have another portfolio with two assets, Asset A and Asset B, as follows:

|

Asset |

Returns (E(Ri)) |

Risk (σi) |

|

A |

10% |

15% |

|

B |

15% |

20% |

The relationship between the two assets, at different levels of asset correlation, is:

|

Weight in Asset A |

Portfolio Return |

Portfolio Risk with Correlation of |

|||

|

1 |

0.5 |

0.2 |

-1 |

||

|

0 |

15.00% |

20.00% |

20.00% |

20.00% |

20.00% |

|

0.1 |

14.50% |

19.47% |

17.91% |

16.97% |

13.23% |

|

0.2 |

14.00% |

18.94% |

16.17% |

14.51% |

7.86% |

|

0.3 |

13.50% |

18.42% |

14.79% |

12.60% |

3.88% |

|

0.4 |

13.00% |

17.91% |

13.76% |

11.26% |

1.29% |

|

0.5 |

12.50% |

17.41% |

13.08% |

10.48% |

0.09% |

|

0.6 |

12.00% |

16.91% |

12.76% |

10.26% |

0.29% |

|

0.7 |

11.50% |

16.42% |

12.79% |

10.60% |

1.88% |

|

0.8 |

11.00% |

15.94% |

13.17% |

11.51% |

4.86% |

|

0.9 |

10.50% |

15.47% |

13.91% |

12.97% |

9.23% |

|

1 |

10.00% |

15.00% |

15.00% |

15.00% |

15.00% |

The above information, when plotted on a graph, would look like this:

Diversification of Portfolio Risk

The portfolio risk can be reduced through diversification by the use of differently correlated assets as follows:

a. Making an investment in a variety of assets. The diversification could be achieved by mixing a variety of assets such as stocks, bonds, cash, real estate, etc. Within the stocks, diversification could be made across the sectors such as energy or consumer goods, large-cap stocks, and small-cap stocks. The bonds could also be diversified by investing in government versus corporate bonds, etc.

b. The portfolio could also be diversified by the use of index ETFs. This also minimizes the cost of diversification.

c. Cross-border diversification can also help in reducing the risk through exposure to different countries and different phases of the business cycle.

d. The key to reducing the risk through diversification is not investing in the own employer’s stocks. The pension plan should also not own the sponsor’s stock as well. This increases the concentration of risk.

e. For the purpose of diversification, the assets should be added to the portfolio only if the risk-adjusted return benefits the portfolio. That is,

f. Another way of reducing the risk is through buying the insurance and the put options.