LOS A requires us to:

describe the portfolio approach to investing

a. The basic principle of a portfolio approach to investing is to select the securities with respect to their contribution characteristics to the whole portfolio, instead of investing in the individual securities and evaluating each in isolation.

All the investors have return objectives along with a certain limit of risk tolerance.

Different assets can be combined in a portfolio to attain the desired investment objective.

b. For making an investment in a portfolio, any investor should go by the following two rules:

i. When there are two assets with the same level of returns, the asset with a lower level of risk should be selected for investment.

|

If, [E(RA) = E(RB)] But, [E(RA) < E(RA)] Then, A is a superior portfolio. |

ii. When there are two assets with the same level of risk, the one with a higher return should be selected.

|

If, [(σA) = (σB)] But, [E(RA) > E(RA)] Then, A is a superior portfolio. |

The main objective of portfolio management, however, is reducing risk rather than increasing the returns.

c. There are two types of risk: systematic risk and unsystematic risk.

The systematic risk of a security is the variance of that security’s return that stems from the overall market movements and is measured by beta. This is a non-diversifiable risk.

The unsystematic risk, on the other hand, is the portion of security’s total risk that is not related to movements in the market portfolio and hence can be diversified.

The portfolio approach provides the benefits of diversification that helps in reducing the non-systematic risk in the investment.

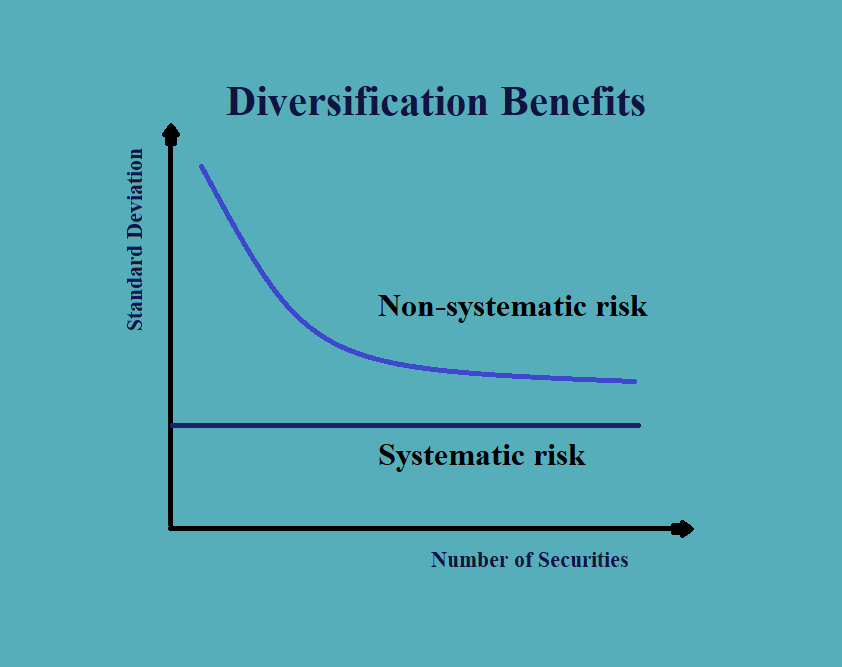

The diversification benefits that can be achieved through diversification can be explained through the following figure:

As can be seen from the above figure, the non-systematic risk of a portfolio, as measured by its standard deviation, tends to decrease as the number of securities in the portfolio increases.

d. The benefits of diversification, as provided by the portfolio approach, can be measured by the diversification ratio. The diversification ratio is the ratio of the standard deviation of the equally weighted portfolio and any random component of that portfolio. The lower the diversification ratio, the better are the benefits of diversification.

|

Where, σP = standard deviation of the equally weighted portfolio. σR = standard deviation of random component. |

e. Thus, the following need to be noted about the portfolio approach to investment:

i. The portfolios may offer equivalent returns with the lower volatility of returns in comparison to the individual securities. This is the most important benefit of this approach.

ii. In the portfolio approach, the asset class selection i.e. weighing each security in the portfolio is more important than selecting the individual securities.

f. The impact of class selection in the portfolio approach can be explained with the help of the following example:

Suppose the returns earned by two portfolio managers in comparison to the returns on the benchmark index were as follows:

|

|

Index |

Manager A |

Manager B |

|

Cash |

10% |

11% |

9% |

|

Fixed Income Securities |

6% |

8% |

4% |

|

Equities |

25% |

30% |

20% |

It can clearly be seen from the above table that manager A is earning above-normal returns and manager B is underperforming.

Now suppose the asset mix of each of the asset class is as follows:

|

|

Manager A |

Manager B |

|

Cash |

5% |

5% |

|

Fixed Income Securities |

60% |

20% |

|

Equities |

35% |

75% |

Now the total return earned by each of the managers, if they invested $ 1,000,000 in the portfolio, would have been as follows:

|

|

Manager A |

Manager B |

|

Cash |

$ 5,500 |

$ 4,500 |

|

Fixed Income Securities |

$ 48,000 |

$ 8,000 |

|

Equities |

$ 105,000 |

$ 150,000 |

|

Total |

$ 158,500 |

$ 162,500 |

We can see from the above that even though manager B is underperforming in the terms of return on each asset class, but when it comes to the total return the manager B is certainly the better performer.

g. There are certain limitations to the portfolio approach. They are:

i. The portfolio approach cannot eliminate the systematic risk.

ii. In the adverse markets all the correlations move towards 1, and thus, the diversification does not provide downside protection.