LOS F requires us to:

describe mutual funds and compare them with other pooled investment products.

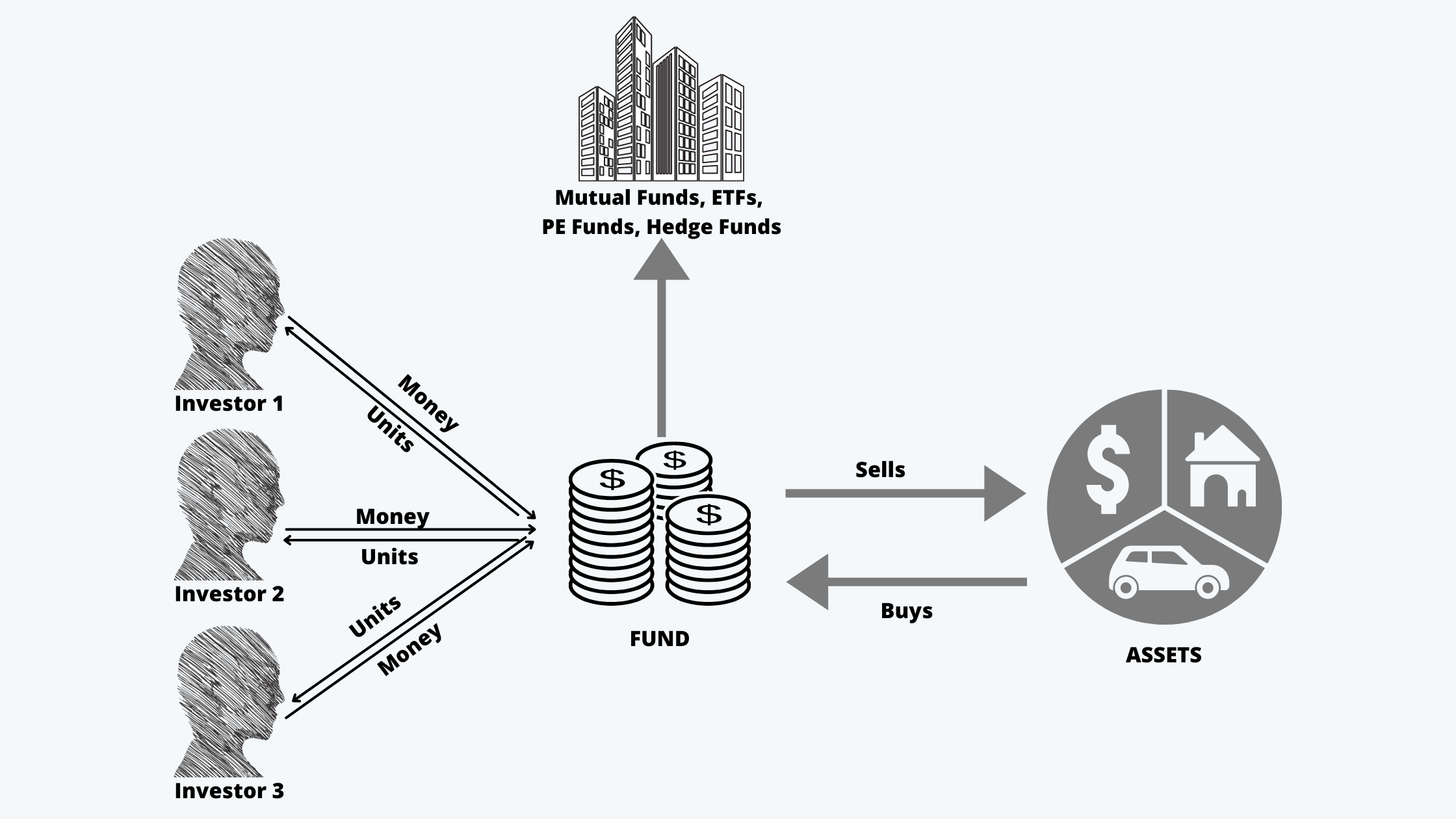

Pooled investments are the managed funds where different investors pool their funds and receive units of the fund asset in return. The fund sells and buys the assets.

The pooled investment funds could be in the form of mutual funds, exchange-traded funds, hedge funds, and private equity funds.

The mechanism of a pooled fund can be explained with the help of the following figure:

Different types of pooled funds are discussed below:

1. Mutual Funds

a. A mutual fund is a professionally managed investment scheme, mainly for individual and institutional investors, providing diversification benefits to them.

b. All the income of mutual funds flows through to the unitholders. Either the holders receive the cash or the income so generated is reinvested.

c. The value of the fund is its net asset value, i.e. NAV. It is calculated on the daily basis, usually at the close of the day.

d. Mutual funds may be of two types: open-ended funds and closed-ended funds.

e. The open-ended funds accept new funds and issue new units at the NAV, and redeem all the units at NAV during the life of the funds. These funds must, therefore, have ready liquidity. And, 100% of the fund amount cannot be invested.

f. A close-ended fund, on the other hand, has a fixed number of units or shares. These units are traded on the exchanges at a premium, discount, or at NAV.

g. The mutual funds may also be categorized as load funds and no-load funds.

h. A load fund has an annual fee charge to run the fund plus a buy or sell commission.

i. In a no-load fund, there is just an annual fee based on the NAV of the assets under management. There is no buy/sell commission on such funds.

j. The mutual funds may also be of the following types:

i. Money Market Mutual Fund. These may be tax-free or taxable.

ii. Bond Funds. These funds hold the bonds and preferred shares as assets.

iii. Equity Stock Funds. These funds hold equity or indices as assets.

iv. Hybrid or Balanced Funds. These funds hold both stocks and bonds as assets.

k. The mutual funds may be actively managed or passively managed.

l. The actively managed funds have a higher management expense ratio (MER). These funds mainly attempt to outperform or beat the benchmark. These funds have higher turnover, faster capital gains realization

m. The passively managed funds, on the other hand, have lower MERs. These funds generally attempt to match the benchmark and have relatively lower turnover and capital gains realization.

2. Exchange Traded Funds – ETFs

a. These are a type of pooled investments in the form of a fund, which issues shares that are traded on an exchange.

b. These funds have a passive management style and are designed to track some asset class or index. And, since it is passively managed, the management cost of such funds is also usually very low.

c. The price of the ETFs is generally very close to its NAV, thus, it carries a very low risk in comparison to the other funds.

d. The exchange-traded funds are very similar to the index mutual funds, except for the following differences:

i. The ETFs have low MERs but do carry a brokerage cost. On the other hand, the index mutual funds do not have brokerage costs but a higher MER.

ii. The ETFs are traded in the open market and are continuously priced, whereas, index MFs are traded out of the fund and are priced once daily.

iii. The investors can take a short position on or hold the ETFs on margin, but for the index MFs, the investors can go long only.

iv. The ETFs generally pay dividends, which give a tax advantage to the investors, in comparison to the index MFs which reinvest the profits, thus providing only the capital gains to the investors.

3. Separately Managed Account

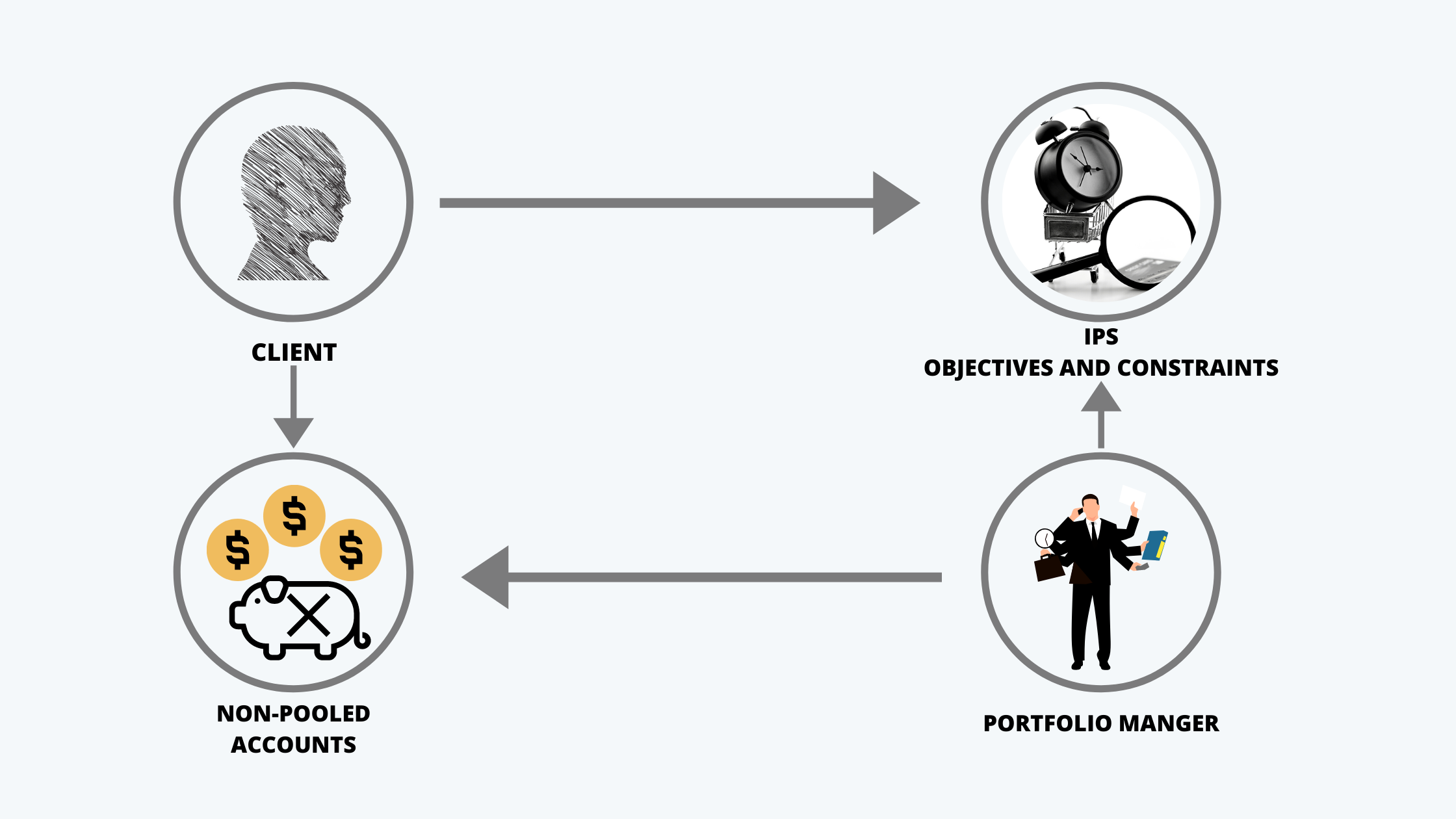

a. The separately managed accounts are also called the wrap accounts.

b. In this scheme of investment, the investor/client opens a separate account which is managed by the portfolio manager. The client specifically provides the objectives and the constraints on the investment through the IPS or the investment policy statement.

The following diagram depicts the mechanism of the SMAs:

c. The investments in a separately managed account are non-pooled; therefore, the client actually owns the assets. Therefore, there is more control over the timings of capital gains.

4. Hedge Funds

a. Hedge funds are the alternative investments that employ different strategies with an objective to earn absolute (not relative), positive, and alpha returns for their investors.

b. These funds make use of different strategies such as convertible arbitrage, dedicated short-bias, fixed-income arbitrage, emerging market investment, equity market neutral, event-driven strategy, global macro, short-selling, leverage, derivatives, etc.

c. The main features of hedge funds are:

i. They are mostly exempt from the stringent regulatory requirements in respect to reporting etc.

ii. Hedge funds are mainly for accredited investors and not for general investors.

iii. The investment in hedge funds may have a lock-up period or fixed redemption dates.

iv. These funds generally carry a management fee plus a performance fee.

v. Additionally, the hedge funds may also have a hurdle rate and a high watermark.

5. Buyout and Venture Capital Funds

a. The LBOs or leverage buyout funds buy the public companies, restructure them, and make an exit from the investment through a re-IPO. In all these transactions, a significant amount of debt is used.

b. The VC or Venture Capitalists provide the financing to the startups.

c. Both LBOs and VCs take an active role in the management of the companies they are investing in.

d. The most critical part of the operations of these funds is the exit, as all the investments they make are mostly illiquid.