LOS G requires us to:

describe methods for measuring and modifying risk exposures and factors to consider in choosing among the methods

1. Measures of Risk Exposure

There are different metrics to measure the risk exposure of a portfolio. Some of the measures for the risk exposure are:

1.1. Risk Metrics

The risk metrics that can be used to measure risk exposure are:

a. Probability,

b. The standard deviation of the portfolio,

c. Beta, which is a measure of systematic risk.

1.2. Derivative Metrics

Some of the derivative metrics to measure the risk exposures are:

a. It is the rate of change of price of the derivative with respect to the price of the underlying assets.

b. It is the rate of change of delta with respect to the rate of change of price of the underlying asset.

c. It is the rate of change of price of the derivative with respect to its volatility.

d. It is the rate of change of price of the derivative with respect to the risk-free rate.

1.3. Bonds

The risk exposure to the bonds is measured with the help of its duration.

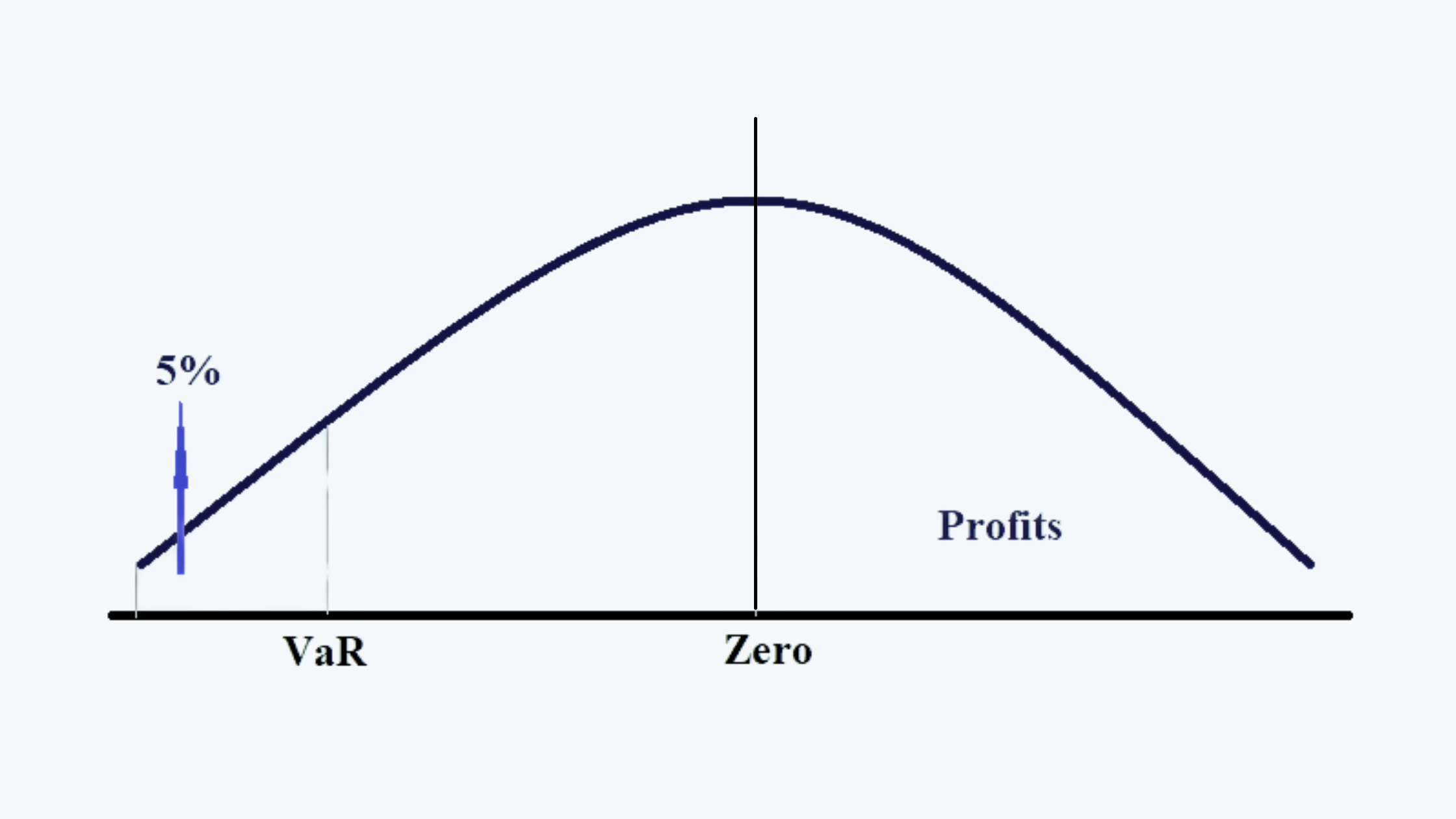

1.4. Value at Risk (VaR)

a. VaR is a statistical measure of maximum potential loss from uncertain events in the normal business over a particular time horizon. It is the maximum loss that a portfolio of securities can face over a specified time period, with a specified level of probability.

b. It is measured in the unit of currency through a probability level. It is the loss measurement consistent with a confidence limit such as 95%, on probability distribution (usually a normal distribution), implying that this is the measurement of a loss that has a chance of only 5% being exceeded.

c. For example, a VaR of $ 1 million for one day at a probability of 5% means that the portfolio of traded securities would expect to lose at least $1 million in one day with a probability of 5%. Alternatively, there is a 95% probability that loss from the portfolio in one day should not exceed $1 million.

This can be expressed diagrammatically as follows:

d. Since VaR must assume a distribution of profits, it is subject to the model error.

e. The extreme value theory attempts to overcome the left-tail shortcomings of the normal distribution.

1.5. Other Measures

The other measures for measuring the risk exposure are:

a. Scenario Analysis. This is sometimes also called stress testing. This is used to complement VaR.

b. Credit Ratings or Credit Default Swap Pricing. These are measures to evaluate risk exposure in the credit markets.

c. Others. Such as operational, compliance, and legal. These methods are difficult to quantify and make use of subjective measures.

2. Risk Modification

a. The risks can be avoided or prevented by avoiding those risks where the associated activities are not worth pursuing. For example, a trader may choose to hedge its exposure instead of speculating the position.

b. An alternative to risk avoidance is risk acceptance. The risk can be accepted through the following measures:

i. Self Insurance. It is a method of keeping the risk exposure that may be too costly to eliminate but using the internal means for reducing the fallout.

ii. Diversification. This reduces the non-systematic risk of the portfolio.

iii. Risk Transfer. This can be done, typically in the form of an insurance policy, where a premium is paid to protect against the loss.

The insurers can also transfer the risk with the help of the re-insurance of CAT bonds.

There are other transfer devices such as surety bonds, fidelity bonds, indemnity clauses, etc.

c. The risk can also be modified through risk shifting. This changes the distribution of risk outcomes