LOS E requires us to:

calculate and interpret beta

Before we get to explain and calculate beta, we first need to understand what a Security Market Line or SML is.

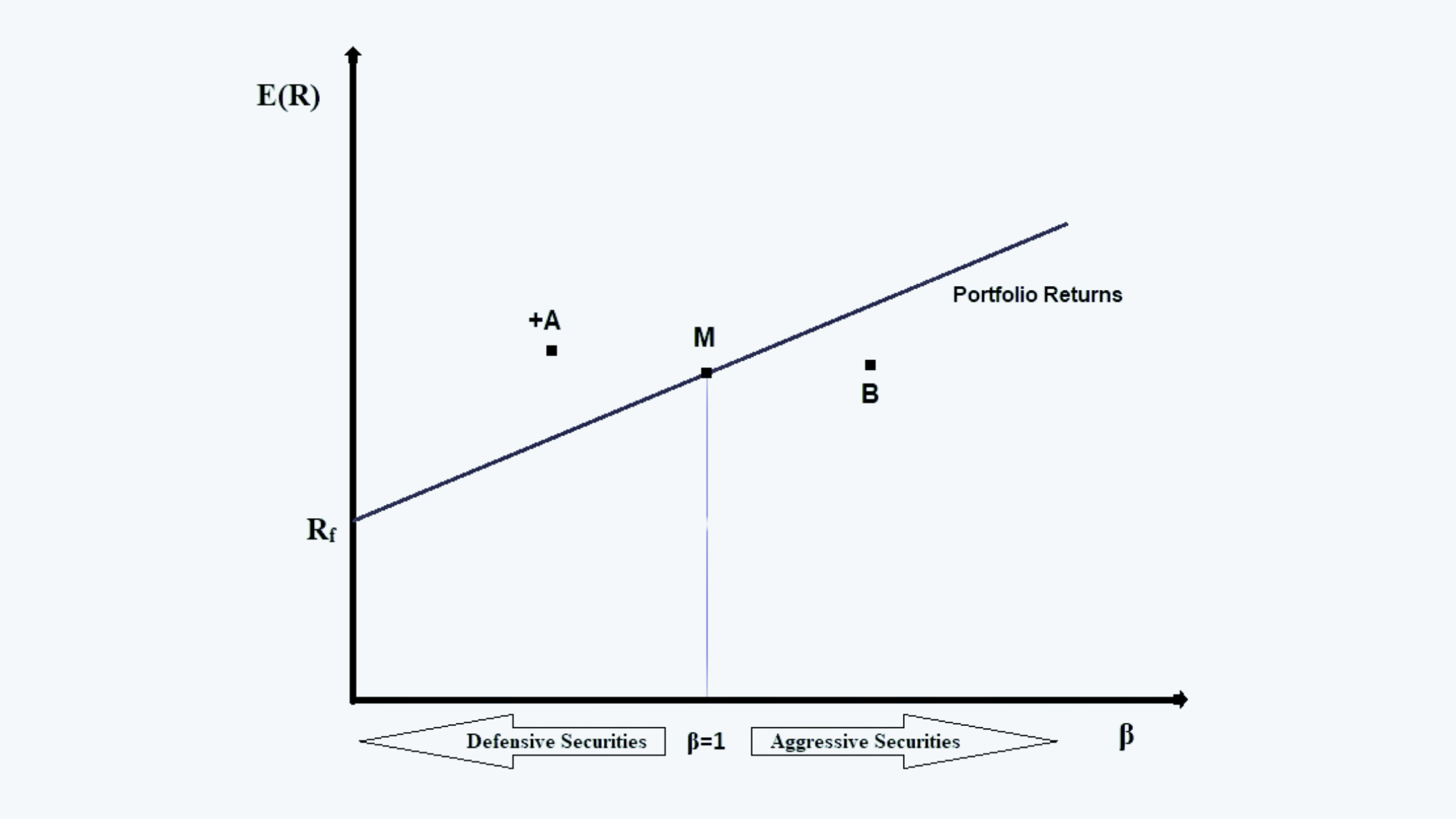

Security Market Line

The security market line or the market line is another way to a perceived risk-return equilibrium relationship. With expected return on X-Axis and β on Y-axis, if the market portfolio is drawn and the line is extended to the risk-free rate of return, SML is obtained.

The equation of the SML is:

There are two instant interpretations of SML:

a. Each asset may be viewed as a combination of the risk-free asset and the market

b. Under equilibrium, all the assets are plotted on the SML i.e., all the assets, which are priced correctly, lie on SML.

Both risk-free rates and the expected return on the market change as the economic conditions change, therefore, the slope of the SML also changes. And, the slope of the SML is equal to the market price of risk.

Beta

a. If we recall the equation generated in the previous model, the return on a security is calculated as follows:

Ri = α + ꞵRm + ɛi

Where α = (1 – ꞵi) rf, which is a constant.

b. A measure of systematic risk could be the covariance of security with the market. So, if we take the covariance of the return on security with the market, the equation would be:

Cov(Ri, Rm) = Cov(ꞵiRm + ɛi, Rm)

Since the first term of the above equation i.e. α is constant therefore its covariance would always be zero.

This equation can be expanded as follows:

Cov(Ri, Rm) = Cov(ꞵiRm, Rm) + Cov(ɛi, Rm)

or

Cov(Ri, Rm) = ꞵi Cov(Rm, Rm) + Cov(ɛi, Rm)

Since the covariance of the market with the market is nothing but the market variance, and έi is the standard error, so its covariance with the market is zero; thus, we can write the above equation as:

Cov(Ri, Rm) = ꞵi σm2 + 0

Therefore, from the above equation, we get the value of beta, which is:

As we know that Cov(Ri, Rm) = ρim σi σm. Therefore, we can rewrite the above equation as:

Or,

That was the derivation of beta.

c. Beta is a measure of how sensitive an asset return is to the market as a whole. It captures an asset’s systematic risk.

d. The average beta of the stocks in the market is always one. This is mainly because, if we insert the value of markets instead of the securities in the equation of beta, we would get the following:

Since the correlation of market with the market is always one, therefore:

ꞵm = 1

Also, it has been noticed that most of the securities in the market also have a correlation with stocks greater than 0.70.

e. We can thus calculate the value of beta, if:

i. we have an estimate of the standard deviation of the security, i.e.σi,

ii. we have an estimate of the standard deviation of the market, i.e.σm, and

iii. we have a value for the correlation between the market return and that of securities.

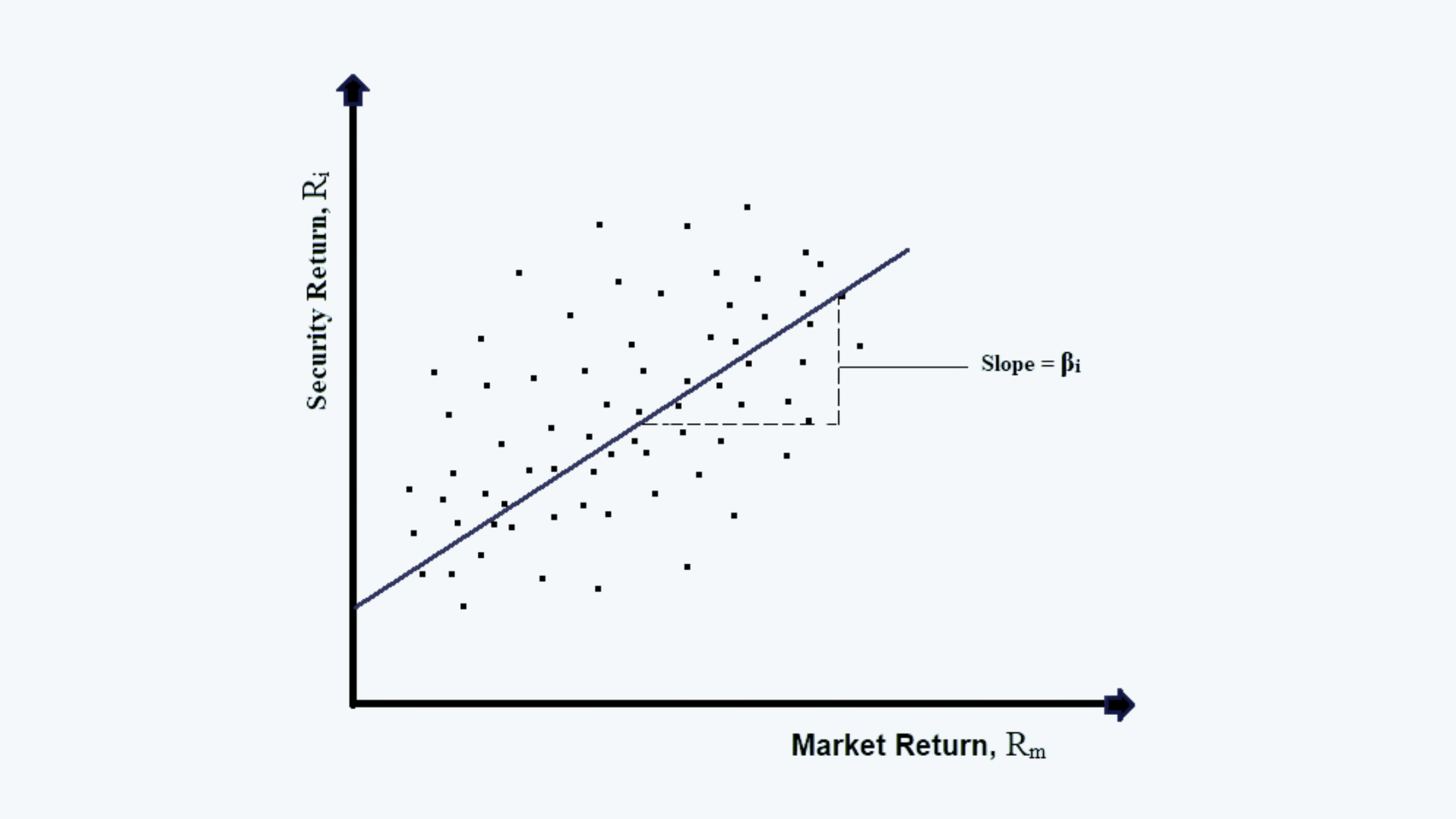

f. The one mentioned above was the statistical way of calculating beta. Beta can also be calculated in a simpler way, which is by plotting the combinations of asset’s return and the market returns on a graph, and then drawing a line through all the points such that it minimizes the sum of squared linear deviations from the line, as follows:

The slope of the line, so drawn is the beta estimate.