LOS F requires us to:

explain the capital asset pricing model (CAPM), including its assumptions, and the security market line (SML)

a. Capital Asset Pricing Model or CAPM is a single index model that describes the relationship between systematic risk and expected return on an asset.

b. The basic equation of the CAPM is:

1. Assumptions Behind CAPM

The basic assumptions behind CAPM are:

a. The investors are assumed to be:

i. utility-maximizing,

ii. risk-averse, and

iii. rational.

b. The markets are assumed to:

i. be frictionless,

ii. have no transaction costs, and

iii. tax-free.

In short, the borrowing and lending transactions are assumed to be taking place at a risk-free rate.

c. All the investors are assumed to be having the same single-period investment horizon.

d. The investors have homogeneous expectations; that is why they arrive at the same valuation for any given asset.

e. All the investments are infinitely divisible. That is, the investors can invest as little as and as much as they want.

f. The investors are the price takers, and no investor is large enough to influence the prices

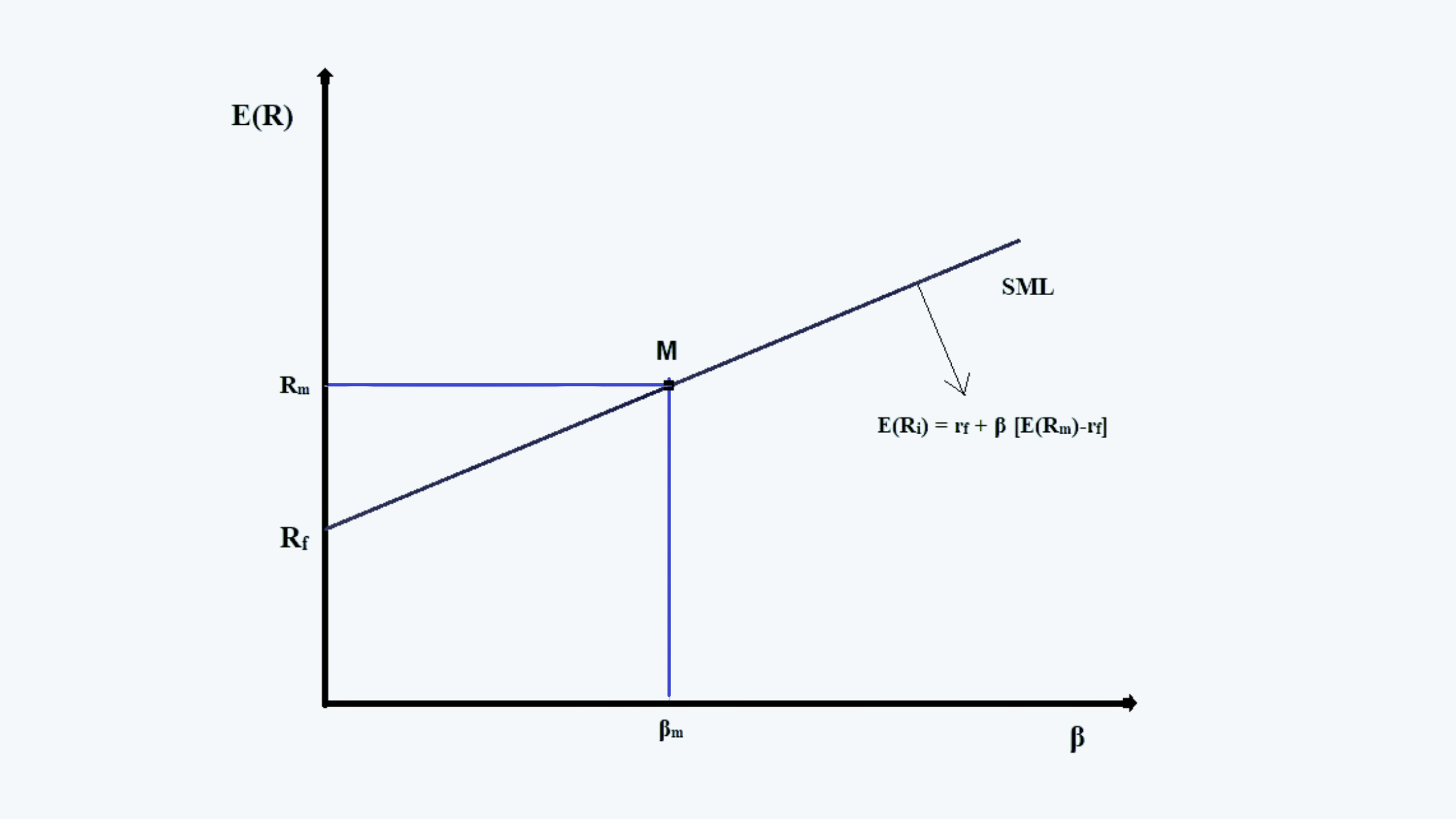

2. CAPM & SML

We have seen above, how to draw a security market line, on similar lines with the capital market line. The equation of the SML is the equation of CAPM.

Following diagram shows the SML and the CAPM equation: