LOS A requires us to:

calculate and interpret major return measures and describe their appropriate uses

a. All the financial assets have two characteristics in common:

i. an expected return, and

ii. uncertainty regarding that return, i.e. risk.

Therefore, all the financial assets can be described by risk and return.

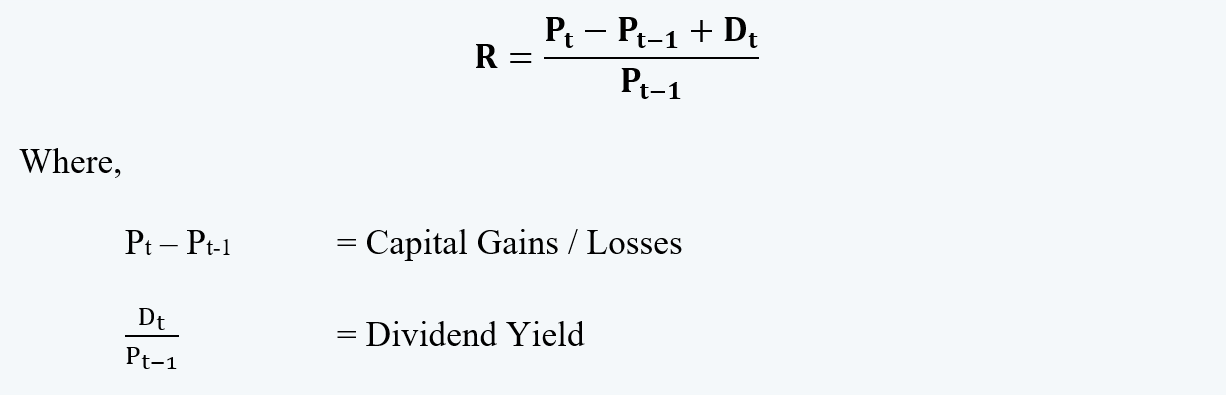

b. The return is typically derived from two sources, i.e. income and capital gains or losses.

c. Thus the total holding period returns from a financial asset are:

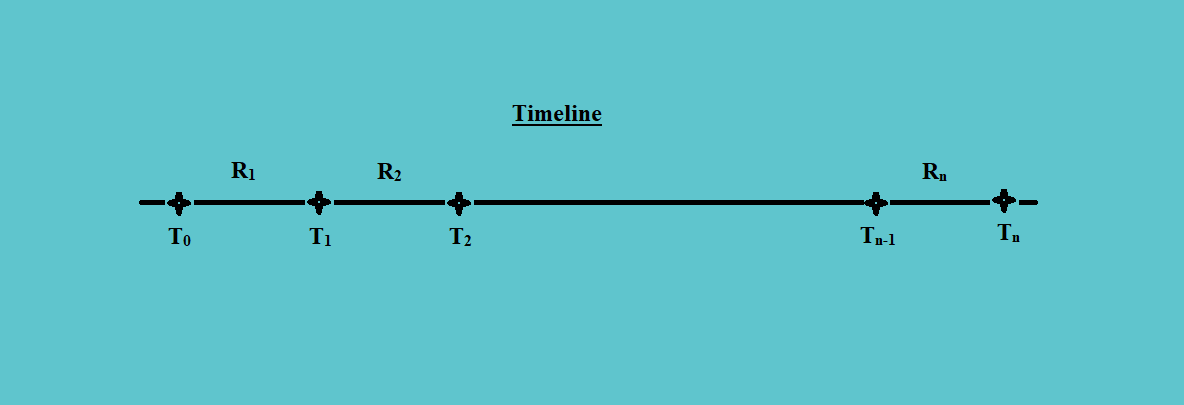

If, however, the asset is held for multiple periods, starting from T0 to T1, T2, up to Tn, and the returns during each of such period where R1, R2, up to Rn, as follows:

Its total holding period returns can be calculated as follows:

For multiple holding periods, the returns could also be measured using the arithmetic mean. This method assumes that there is no compounding effect. This method gives us only an average return over a given random one-period timeframe.

So, if an asset is held from T0 to T1, T2, up to Tn, and the returns during each of such period were R1, R2, up to Rn, as follows:

Its total average returns can be calculated as follows:

Another way of calculating the returns on an investment held for multiple periods is the geometric mean. This method considers compounding and represents growth over a given time period.

So, if an asset is held from T0 to T1, T2, up to Tn, and the returns during each of such period were R1, R2, up to Rn, as follows:

Its total average returns can be calculated as follows:

This can also be written as:

d. We can also calculate the returns on the financial asset by calculating the money-weighted returns. It is also called the internal rate of return or IRR. It is the rate at which the present value of both the cash outflows and inflows equals zero. It is the rate of return generated by the asset internally.

This method accurately reflects what a specific investor earned, but this method lacks comparability.

For, an asset with the holding period is T, having different cash flows such as CF1, CF2, up to CFT, the IRR would be calculated by equating the sum of the present value of such cash flows with zero. That is,

e. For example, if we invest $ 1 million at the beginning of a 5 year holding period, and the annual returns during these 5 years were as follows:

|

Year |

Percentage Return |

|

1 |

10% |

|

2 |

-5% |

|

3 |

10% |

|

4 |

15% |

|

5 |

10% |

i. The holding period return from the investment would be:

= [(1+0.10)(1-0.05)(1+0.10)(1+0.15)(1+0.10)] – 1

= 0.4541 or 45.41%

ii. The arithmetic mean or average return would be:

= (10 – 5 + 10 +15 + 10)

= 8%

iii. The geometric return of the investment is:

= [(1 + 0.10) (1 – 0.05) (1 + 0.10) (1 + 0.15) (1 + 0.10)]1/5 – 1

= 0.0778 or 7.78%

iv. For calculating the money-weighted returns, assuming that the income earned on the investment was reinvested, the cash flow and the closing balance of investment at the end of each year would be:

|

Year |

Cash Flow |

Income |

Closing Balance |

|

0 |

(1,000,000.00) |

– |

1,000,000.00 |

|

1 |

– |

100,000.00 |

1,100,000.00 |

|

2 |

– |

(55,000.00) |

1,045,000.00 |

|

3 |

– |

104,500.00 |

1,149,500.00 |

|

4 |

– |

172,425.00 |

1,321,925.00 |

|

5 |

1,454,117.50 |

132,192.50 |

– |

v. Now, with the available figures of cash flow, we can calculate the IRR using the financial calculator.

IRR = 7.78%

Thus the money-weighted return is 7.78%

f. Following is the interpretation of the different returns as calculated above:

i. The holding period return is the return on investment for the period of the full five years. This return is only useful for comparing the returns of investors with a similar holding period.

ii. The arithmetic return is the average of different returns earned during the investment period. It only gives a guess, as to what an average return, during any one period of investment could possibly be.

iii. The geometric mean gives us the compound annual return earned during any of the investment periods.

iv. The money-weighted return, on the other hand, shows the actual one-period return generated by the asset during its holding period.

g. If we are given the returns for a certain period during the day, we can annualize the same using the following formula:

For example, if an asset earned a 0.15% return for a 7-day holding period, its annualized return would be:

= [(1 + 0.0015)365/7] – 1

= 0.0813 or 8.13%

h. If we have to compare the returns on different assets or portfolios held for different time periods, it is always desirable to convert such returns into annualized returns, for uniformity of comparables.

However, contrary to what is reflected by the figures of annualized return that we can earn these returns consistently, these returns may not be capable of replicating consistently throughout the year. The returns may also be seasonal.

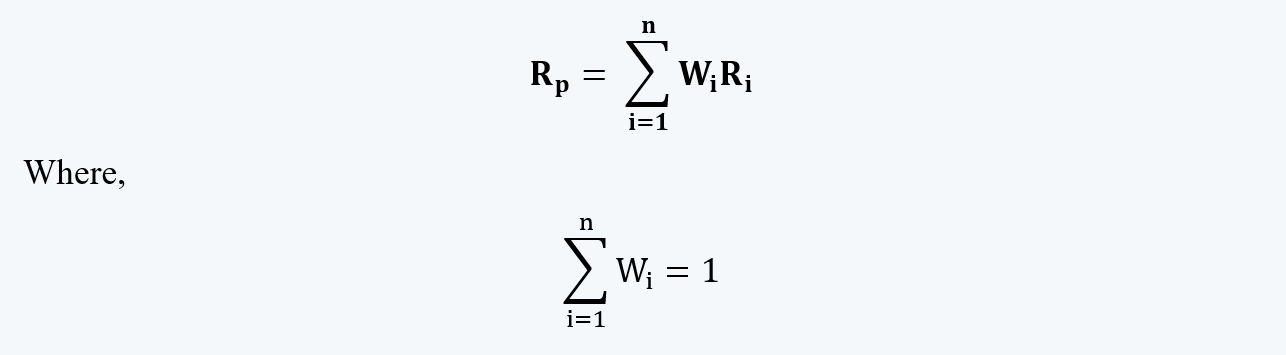

i. These were the methods used to measure the returns of the individual assets within the portfolio. The portfolio return can be measured by calculating the weighted average of the returns of individual assets within the portfolio.

j. The other return measures for the assets and portfolio are gross returns and net returns, pre-tax and post-tax returns, nominal and real returns, levered and unleveraged

i. Gross Returns are the returns earned by the portfolio before charging the management, administration, and other fees. Gross returns are the basis for comparing the manager’s performance.

ii. Net Returns, on the other hand, are the returns actually receivable by the investors. The management, administration and all the other cost that is chargeable from the investor is deducted from the gross returns to calculate the net returns.

iii. For understanding the pre-tax and post-tax returns, it is important to understand the components of capital gains.

The capital gains could be of two types, the short-term and long-term. Long-term capital gains usually receive preferential tax treatment in comparison to short-term capital gains.

There could also be two kinds of income from the investments, i.e. interest and dividends. Dividends also receive preferential tax treatment.

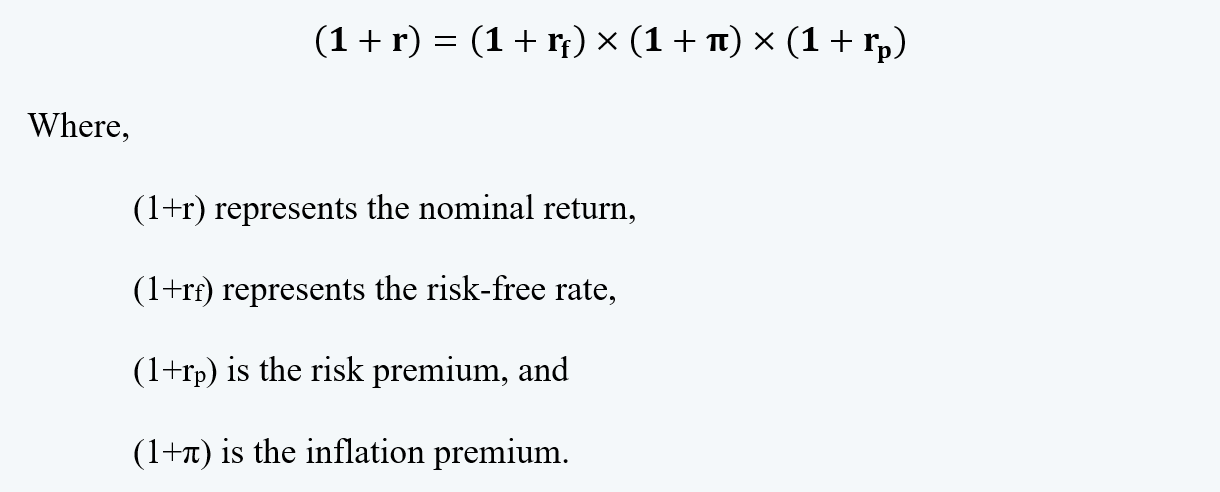

iv. The returns could also be real and nominal.

The nominal returns are the returns quantified in the present-day monetary terms. Whereas, the real returns are the inflation-adjusted returns earned by the investors.

They are the returns in terms of the purchasing power of the investors.

The relation between the real and nominal returns can be written as follows:

v. The leveraged returns are earned either by the use of derivatives or margins. The effect of leveraging magnifies both the gains and the losses. The leveraged returns must account for the margin loan interest