The term hedge fund is defined as any pooled investment vehicle that is privately organized and administered by professional investment managers and is not offered to the general investors.

1. Characteristics of Hedge Funds

Some of the important characteristics of a hedge fund are:

1. They are usually organized as a limited liability partnership. This helps in alignment with the interest of management and investors.

2. Hedge funds employ dynamic trading strategies that involve a frequent change of stances in different assets markets such as identifying the mispricing between the markets and changing the strategies to take advantage of such situations.

3. Hedge funds usually have highly skilled, specialized, and experienced fund managers.

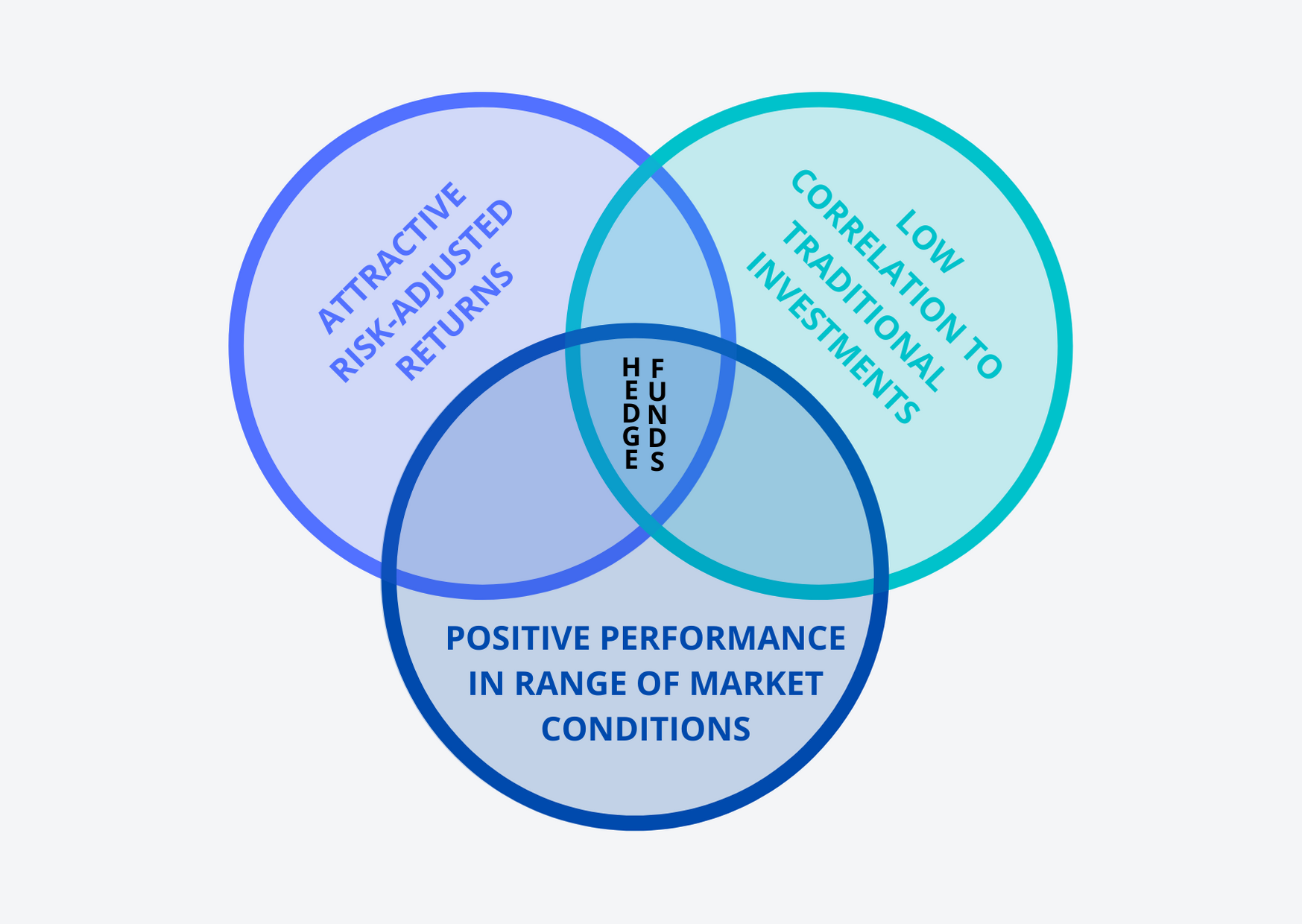

4. The performance of most hedge funds is independent of the direction of trends in traditional investments such as equity, bonds, mutual funds, etc.

5. Hedge funds have a high floor limit to the investment, thus attracting only high net-worth and institutional investors.

6. Hedge funds are relatively illiquid investments.

7. There is a high degree of leveraging in the hedge funds investment.

8. This market is characterized by a lack of transparency and a regulatory framework.

9. The return objective for a hedge fund is usually stated either on an absolute basis (e.g. 10%) or a relative basis (such as 5% above a certain benchmark).

2. Investment Strategies in Hedge Funds

There are basically four categories of strategies that are followed by the hedge fund managers to manage their investments. They are:

2.1. Event-Driven Strategies

These strategies are solely focusing on the events of the corporate life cycle for investment. They involve significant opportunities created by corporate events such as distressed debt investing, mergers and acquisitions, share buyback, corporate spin-offs, demerger, restructuring, etc. Managers may employ derivative instruments to protect themselves from downside risk involved in such investment through options contracts on the underlying company stock. Some of the important event-driven strategies are:

1. Merger Arbitrage. This strategy involves the purchase of securities of the company being acquired and selling that of the acquiring company or reverse position in anticipation of the failure of the proposed deal.

2. Distressed/Restructuring. This strategy involves buying and occasionally shorting securities of the companies that have filed for bankruptcy or firms going for restructuring. The fund tries to profit from the expected price movement of securities.

3. Activist Shareholders. This strategy involves buying sufficient equity shares to influence a company’s policies to increase company value.

4. Special Situation. This strategy involves investing in the securities of a firm that are issuing or repurchasing securities, spinning off divisions, selling assets, or distributing capital, etc.

2.2. Relative Value Strategy

These are also known as non-directional strategies. They attempt to locate profit relative pricing discrepancies between instruments such as equity, debt, options, and future. Many hedge fund strategies employ these strategies with leverage and look for opportunities globally. Some of the relative value strategies are:

1. Convertible Arbitrage Fixed Income. These strategies exploit pricing discrepancies between convertible bonds and the common stock of issuing companies.

2. Asset-Backed Fixed Income. This strategy exploits the differences amongst the prices of asset-backed securities or mortgage-backed securities.

3. General Fixed Income. This strategy tries to make a profit out of the price discrepancies between fixed-income securities of different types.

4. Here the managers try to make a profit out of the differences in the option prices and the manager’s expectation of prices in the future.

5. Multi-Strategy. This strategy aims to exploit the price differences amongst different asset classes and markets.

2.3. Macro Strategy

Macro strategies involve making an investment decision based upon the macro-economic and global trends and events.

2.4. Equity Hedge Fund Strategy

These are the most popular form of strategy amongst hedge funds. These strategies involve the combined purchase and sale of two securities of a similar sector, going long on the undervalued one and short on the undervalued stock. Some of the equity hedge fund strategies are:

1. Market Neutral. This strategy involves making use of both fundamental as well as technical analysis to identify the undervalued and overvalued stocks. The stocks so-identified as undervalued are held long and those identified as overvalued are held short.

2. Fundamental Growth. This strategy involves identifying the stocks with high expectations for growth through fundamental analysis. The stocks with high expectations of capital appreciation in the future are acquired and held for longer term.

3. Fundamental Value. According to this strategy, the stocks that are undervalued are identified through fundamental analysis and are held long.

4. Quantitative Directional. This strategy is like market neutral strategy, where both undervalued and overvalued stocks are identified to be held long and short respectively. The only difference here is that this strategy employs only technical analysis for the purpose instead of both technical and fundamental analysis.

5. Short Bias. This strategy concentrates on the net short side of securities on the expectation that the market will decline. Thus, this strategy employing a short position on the overvalued securities and a lesser longer position.

3. Benefits of Hedge Funds

1. Most hedge funds have the potential to generate positive returns in both rising and falling equity and bond markets.

2. The inclusion of hedge funds in a portfolio makes it balanced by reducing overall portfolio risk and volatility and increasing returns.

3. Due to the existence of a huge variety of hedge funds and their investing strategies, the investors get a lot of options to choose from that meet their investment objectives.

4. Records show that hedge funds have exhibited higher returns and lower overall risk than traditional investments.

5. The expertise of the fund manager reduces the overall burden of correctly timing the entry and exit from the asset.

4. Risk with Investing in Hedge Funds

The lack of correlation between hedge funds and traditional investments reduces the overall risk and increases the overall return. But, the records have shown a positive correlation with the market during periods of the financial crisis. This increases the potential downside risk of investing in hedge funds.

5. Valuation of Hedge Funds

1. A hedge fund is valued based on the value of the underlying assets.

2. So, for those underlying assets that are traded on an exchange, the closing price or the average of bid and ask price at the time of closing is considered for the value of the investment.

3. Whereas, for the non-traded securities their intrinsic value is considered for valuation.

4. Sometimes trading NAV is calculated instead of NAV used for the accounting purpose, where the value of the security is reduced for the degree of illiquidity.

6. Hedge Fund’s Due-Diligence

While investing in hedge funds or any other investment a lot of factors need to be considered. Starting from the investment strategy of the fund to the risk-return profile; they should match the investor’s requirements. Some of the factors that need to be considered are:

1. Investment strategy,

2. Investment process,

3. Historical return,

4. Valuation and returns calculation method,

5. Sources of competitive advantage,

6. Amount of assets under management,

7. Management style,

8. Longevity,

9. Reputation,

10. Growth plan,

11. Systems for risk management, and

12. Appropriateness of benchmarks.